Tax 101: The Problem of Life Insurance

The increasingly favorable tax treatment of life insurance presents a challenge for Biden's proposal to tax gains at death

President Biden’s proposal to tax unrealized gains at death (with a generous $1 million exemption1) is an enormously positive tax policy development. Nothing in this post is meant to suggest otherwise. But there remains a relatively easy workaround that will allow high-net-worth individuals to generate virtually unlimited amounts of investment income while avoiding capital gains taxes during life and at death, notwithstanding the (prospective) reform of stepped-up basis. And it’s literally Tax 101 (i.e., § 101 of the Internal Revenue Code).

The goals of this post are:

To explain the extraordinarily favorable tax treatment of life insurance (virtually every tax lawyer is familiar with § 101 and the nontaxation of life insurance inside buildup, but relatively few of us have drilled down deep into the details);

To highlight little-noticed changes in the insurance tax rules—enacted in December 2020 as part of the $900 billion bipartisan Covid relief package—that supercharge the tax benefits of life insurance; and

To explain why the tax-minimization opportunities offered by life insurance pose a serious challenge to President Biden’s proposal to tax unrealized gains over $1 million at death.

To be clear, stepped-up basis reform is a good idea and will raise a lot of revenue.2 But even with stepped-up basis reform, life insurance will remain a loophole in our capital income tax system that’s big enough to drive the Ever Given container ship through.

[Also: Hi. This is the first post on a substack that will focus primarily on tax law and policy. Back in the days before Substack-style individualism rended group blogs, I posted over on Medium at Whatever Source Derived. Alas, the tax policy conversation appears to be shifting to the newsletter format, so I guess I’ll go with the flow. You can sign up to receive new installments in your inbox. All posts are free.]

The optimal policy solution is to overhaul the tax treatment of life insurance, but unfortunately that probably lies outside the Overton window for now. In later posts, I’ll offer some suggestions for incremental reforms—including reforms that Treasury and the IRS can potentially pursue under existing statutory authority. The first step, though, is to recognize the policy problem (or, from a taxpayer’s perspective, the planning opportunity).

How it works

One way to think about cash-value life insurance is as a combination of (1) a tax-free savings account with no contribution limit and (2) a series of one-year term life insurance policies. To illustrate:

Let’s say I buy a universal life insurance policy with a $1 million death benefit and annual premium payments starting at $10,000 (figures picked purely for illustrative purposes).

In year 1, I deposit $10,000 into the tax-free savings account, and I use a portion of those funds to buy a one-year term life insurance policy with a $1 million death benefit.

To make the math easy, let’s say that the cost of a one-year $1 million term life insurance policy—given my age and health—is $1,000.

In year 1, the insurer charges my account $1,000 for the term policy, leaving $9,000 in my account.

The remaining $9,000 is invested in stocks, bonds, or other assets. For example, a universal life insurance policy might allow me to invest my cash-value account in a stock fund that tracks the S&P 500 (often with a floor that prevents the annual return from falling below zero; sometimes with a cap that limits the return in a bull-market year). A private placement life insurance policy—available to high-income/high-net-worth investors—might offer the opportunity to invest in hedge funds or private equity funds.

Investment income accrues tax-free. So if the year 1 return is 10 percent, my cash value account will grow from $9,000 to $9,900.

In year 2, I pay another premium (i.e., make an additional deposit into the tax-free savings account). My account is charged again for a one-year $1 million term life insurance policy, but now two things change:

First, because I’m a year older, the cost per $1 of insurance protection will rise;

Second, and partly or fully offsetting the first change, I’ll need less insurance protection in order to sustain the same $1 million death benefit. That’s because I’ve already accumulated $9,900 of cash value in my account, which will be paid out when I die. In order to guarantee a $1 million death benefit, I now only need to buy $990,100 of insurance protection (i.e., $1 million minus the $9,900 of cash value that I’ve already accumulated).

As the cash value grows, the net amount at risk (i.e., the difference between the death benefit and the cash value) declines. When the net amount at risk is low relative to cash value, the insurance policy looks more and more like a tax-free savings account and less like a mortality bet.

The biggest tax benefit of life insurance is the nontaxation of inside buildup (i.e., tax-free growth in the cash value account). Under the subchapter L rules, the insurer doesn’t have to pay tax on that investment income (which in isolation makes some sense—the growth in the cash value account isn’t “income” to the insurer because the insurer is obligated to set aside the money for me). And I don’t pay tax either (on the theory that I haven’t actually or constructively received the income yet). Then when I die, my beneficiaries receive the death benefit (including the cash-value component) tax-free under § 101.

On top of that, if I want to withdraw funds from the tax-free savings account before I die, I can do that in a tax-advantaged way. Under § 72, withdrawals from a life insurance policy are taxed on a first-in, first-out (FIFO) basis. In other words, everything up to the amount that I’ve paid in premiums is treated as recovery of basis.

For example, imagine that after year 1, I decide to withdraw half of the $9,900 I’ve accumulated in the cash value account (i.e., $4,950). Under the stacking rules for life insurance in § 72, I’d pay no tax, because $4,950 is less than what I’ve paid in premiums. Compare that to the situation where I buy shares in a mutual fund outside a universal life insurance account for $9,000 and those shares grow to $9,900. If I were to liquidate half of my investment, I’d pay a tax on the amount realized ($4,950) minus my basis in that half of the shares ($4,500).

There are further benefits still. Without withdrawing cash, I can use my insurance policy as collateral for a loan and pay no tax on the loan proceeds. (The life insurer will probably lend directly to me.) And under § 1035, I can exchange my life insurance policy for another life insurance policy (e.g., if another life insurer offers a more attractive menu of investment options) and not pay any tax on the cash value that has accumulated over and above my premiums. This is similar to the § 1031 rules for real estate. But while Biden’s plan would repeal § 1031, it doesn’t touch § 1035.

So why doesn’t life insurance take over the world?

In light of these tax benefits, one might fairly ask: Why doesn’t everyone invest via cash value life insurance (or, at least, every high-net-worth individual who maxes out other tax-free savings opportunities like IRAs, 401(k)s, and 529s)? Wouldn’t the perfect tax shelter be a life insurance policy with a death benefit that fluctuates with the cash value, so that there is no net amount at risk (in which case the policy really would be a tax-free savings account masquerading as insurance)?

(Before we get to that question, note that even though the life insurance industry hasn’t taken over the world, it is really big! At the end of 2019, the total value of cash and invested assets held by U.S. life insurers was $4.6 trillion. Not all of that investment is tax-motivated, but lots of high-net-worth individuals and their financial advisers are certainly aware of the tax benefits of life insurance.)

There are two reasons why cash value life insurance hasn’t taken over the world.

First, you can’t actually have a life insurance policy with a death benefit that exactly equals the cash value. (Actually, you can if you’re over the age of 95, but we’ll get to that in a moment.) Congress in the 1980s enacted an extraordinarily intricate set of requirements that prevent pure investment products from qualifying as life insurance for federal income tax purposes.

Second, high-net-worth individuals don’t need life insurance in order to get the benefit of unlimited tax-free savings. You can, in effect, create your own cash value life insurance policy by purchasing zero-dividend stock. For example, if you buy shares in Berkshire Hathaway (which, incidentally, has a substantial insurance business), none of your investment gains will be taxed during your lifetime because Berkshire Hathaway never pays a dividend. If you want to tap into those gains during your life, you can take out a loan secured by your Berkshire Hathaway shares. And at death, you’ll get stepped-up basis, wiping away a lifetime of gains. (Why pay fees to a life insurer when you can just buy stock in a life insurer?) And it’s not just Berkshire Hathaway: other zero-dividend stocks, like Amazon, Google, and Facebook, effectively offer the same “buy/borrow/die” opportunity for tax-free accumulation.

But . . . the two factors that historically limited the flow of investment dollars into cash value life insurance have changed/are changing. First, Congress in December 2020 substantially relaxed the limits on what can qualify as life insurance, making it much easier for insurers to offer products that look a lot like pure tax-free savings accounts. And second, stepped-up basis reform is now very much on the table, putting the age-old buy/borrow/die strategy in peril.

What changed in December 2020?

To understand the importance of the December 2020 changes, we need to rewind to 1984.

In order to curtail the use of life insurance as a pure tax-free savings vehicle, Congress enacted § 7702 as part of the Deficit Reduction Act of 1984. That provision restricts the range of life insurance policies that can qualify for favorable income tax treatment. To qualify, a policy must meet either (1) the cash value accumulation test or (2) the guideline premium and cash value corridor test. I’ll focus on the second test here, as it appears to be the one that very high-net-worth individuals choose more often for private placement policies. (Once you pick either test, you can’t go back.)

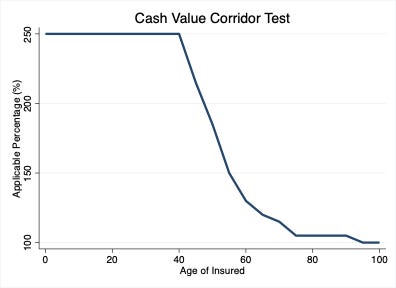

The guideline premium and cash value corridor test has (as the name suggests) two components. The second component—the cash value corridor—is the easiest to explain. Under the cash value corridor, the death benefit must be an “applicable percentage” of the cash value. For example, the applicable percentage is 250 percent when the insured person is younger than 40. So for a policy with a $1 million death benefit, the cash value (the amount in the tax-free savings account) can’t exceed $400,000 until the insured person reaches 40.

As the insured individual ages, the applicable percentage declines. After age 95, the applicable percentage is 100 percent, meaning that the life insurance policy can become a pure tax-free savings account (with no net amount at risk). If the amount in the tax-free savings account bumps up against the cash value corridor limit, the insurer and the policyholder can increase the death benefit so as to remain in compliance with § 7702 (though that will then increase the net amount at risk and so entail a higher cost of insurance protection).

The other component of the guideline premium and cash value corridor test is more involved. It stipulates that the sum of premiums paid under a contract can’t exceed the guideline premium limitation as of that time. The guideline premium limitation has two sub-components:

The first is the guideline single premium, which is the lump-sum amount that—if it were deposited in the tax-free savings account—would be sufficient to fund all of the future one-year term life insurance policies, assuming (per the 1984 statute) that the tax-free savings account earns interest at a rate of 6 percent.

The second is the guideline level premium, which is the annual premium that—if it were paid every year until the insured reaches the age of 95—would be sufficient to fund the entire string of one-year term life insurance policies guaranteed under the contract, assuming (again per the 1984 statute) that the tax-free savings account earns interest at a rate of 4 percent.

These calculations must be based on “reasonable” mortality charges (generally, the 2017 commissioners standard ordinary tables prescribed by the National Association of Insurance Commissioners) and other “reasonable charges … which (on the basis of the company’s experience, if any, with respect to similar contracts) are reasonably expected to be actually paid.”

Pause here to note that these rules are insanely complicated. They also were, at least through 2020, binding constraints on investment-oriented life insurance products. Taxpayers would have to buy a lot of insurance protection (at least at first) in order to take advantage of tax-free growth of cash value. For some high-net-worth individuals, that might be fine—they might want a lot of life insurance. But it’s a bummer if you’re looking to create a life insurance policy that effectively mimics a Roth IRA.

And that’s where the December 2020 Covid relief package comes in. Section 205 of that bill changes the interest rate assumptions that insurers must use when calculating the guideline single and level premiums. For 2021, the guideline single premium rate is 4 percent (instead of 6 percent), and the guideline level premium rate is 2 percent (instead of 4 percent). After 2021, the rates will be floating. The guideline single premium rate will be 2 percentage points above the guideline level premium rate, and the guideline level premium rate will be the lesser of (1) a rate prescribed the National Association of Insurance Commissioners or (2) the applicable federal mid-term interest rate, rounded to the nearest whole percentage point (currently, 1 percent).

A change from 6 percent to 4 percent or from 4 percent to 2 percent might not seem like a lot, but it is. The ceilings imposed by the guideline premium requirements are difficult to calculate because they will vary from insured to insured (on the basis of age and mortality risk) and from insurer to insurer (on the basis of the insurer’s past experience with similar policies). The CEO of one private placement life insurance carrier, Alan Jahde, offers illustrative calculations based a 40-year-old male nonsmoker who wants to fully fund a policy through a series of four consecutive annual lump-sum payments. In that example, for a policy with a $10 million level death benefit under the old § 7702 interest rates, the 40-year-old male could pay in premiums of $368,433 per year for four years before bumping into the guideline premium limitations. Under the new post-December 2020 interest rates, the same 40-year-old male could pay in premiums of $699,986 per year for four years. Remember, the idea is to stuff the life insurance policy with as much cash as possible so as to take advantage of tax-free growth, so a near-doubling of the allowable premium payment is a very good thing from the taxpayer’s perspective.

A further implication of the December 2020 change is that the modified endowment contract (MEC) rules in § 7702A are much less likely to bind. A life insurance policy becomes an MEC if it fails the “7-pay test”—i.e., if premiums paid over the first seven years exceed the total amount that would be needed to fund all future benefits (based on assumptions similar to the guideline premium test). An MEC doesn’t lose the advantage of tax-free savings and exclusion of death benefits, but it does lose the perk of FIFO treatment for cash withdrawals. Moreover, withdrawals from an MEC before age 59 1/2 are generally subject to a 10 percent penalty. All in all, it’s best to avoid MEC status.

The interest rate for § 7702A purposes is the same as the interest rate used for the guideline level payment test in § 7702, so reducing the § 7702 rate mechanically lowers the § 7702A rate. That, in turn, lifts the 7-pay threshold. How much of a difference this makes will depend upon the age of the insured as well as the mortality and expense assumptions baked into the insurer’s calculations. In Jahde’s illustration, the change from a 4 percent rate to a 2 percent rate effectively doubles the amount that a 40-year-old can contribute in the first seven years of a policy without tripping up the MEC rules.

The upshot is that Congress has lowered the guardrails on the use of life insurance as a tax-free savings account at precisely the moment when stepped-up basis reform makes life insurance significantly more attractive as a tax-minimization tool.

How big of a deal is this?

In December 2020, the Joint Committee on Taxation estimated that the changes to the § 7702 rates in the Covid relief package would cost the federal government $3.287 billion over the next decade. That’s not nothing, but it’s not huge relative to the $1.7 trillion per year in individual income tax revenues that the federal government takes in.

But ... the annual cost of the § 7702 rate changes increases over time, as taxpayers are able to accumulate more and more tax-free savings inside life insurance policies. For example, JCT estimated that the annual cost of the changes would approach $1 billion per year near the end of the 10-year budget window (no doubt rising after that).

And these December 2020 projections envisioned a world with the old stepped-up basis rules. If Congress enacts President Biden’s stepped-up basis reforms, the impetus for high-net-worth individuals to shift from other investments to life insurance will increase substantially. In that case, we can expect the revenue loss from the § 7702 changes to increase considerably by the 2030s.

To be clear, the life insurance workaround won’t allow all high-net-worth individuals to avoid the effects of stepped-up basis reform. Taxpayers who already have accumulated significant unrealized gains outside of life insurance policies won’t be able to convert those gains into life insurance cash value (at least not without paying capital gains tax along the way). Moreover, while life insurance allows taxpayers to reproduce the benefits of buy/borrow/die on a going-forward basis, it won’t allow taxpayers to reproduce the benefits of found/borrow/die on a going-forward basis. (In other words, entrepreneurs who hold founders’ stock in startups won’t be able to invest in their own startups through life insurance.) Finally, some high-net-worth taxpayers might balk at the high fees often associated with life insurance (though those fees will seem like less of a drawback if the tax drag on non-life-insurance investments increases dramatically).

Still, life insurance presents a major challenge for efforts to implement a comprehensive capital income tax, because it allows at least some high-net-worth individuals to accumulate virtually unlimited amounts of investment income tax-free. The silver-bullet solution would be to end the tax-free treatment of inside buildup (which President Reagan actually proposed in 1985). But that seems unlikely for three reasons:

First, a huge portion of the U.S. population would be affected. (An estimated 54 percent of U.S. adults own life insurance policies, and while many of those policies haven’t accumulated substantial cash value, the impact of inside buildup taxation would be much broader than, for example, President Biden’s proposal to tax unrealized gains over $1 million at death.)

Second, the transition issues are really tricky. Taxation of inside buildup would upset the interest-rate assumptions upon which existing policies are built, with potentially devastating implications for insurance-company solvency. (The Reagan proposal sought to address this by exempting all existing policies.)

Third, and perhaps most importantly, the life insurance industry wields extraordinary political influence on both sides of the aisle. The industry has employees in every congressional district, and life insurers are among the top donors to many members of the tax writing committees. Serious reform of the life insurance tax rules would require true political courage.

I’ll suggest some more modest reforms in future posts (subscribe to get them in your inbox). For now, thanks for reading >3000 words on life insurance!

Conflict-of-interest disclosures: I own/control <$15,000 of stock in Berkshire Hathaway and Prudential, and <$5,000 of stock in MetLife. In a future post, I’ll explain why holding individual stocks rather than index funds can generate significant tax benefits—especially for taxpayers with charitable-giving goals. I don’t have a universal life insurance policy, though writing this post has convinced me that I ought to consider it.

Further reading: The best article I’ve read on the taxation of life insurance is Andrew Pike, Reflections on the Meaning of Life: An Analysis of Section 7702 and the Taxation of Cash Value Life Insurance, 43 Tax Law Review 491 (1988) (still quite relevant after 33 years!). If you’re interested in the subject, I highly recommend it.

For most high-net-worth individuals, the exemption is effectively $1.25 million ($2.5 million for couples) because Biden would leave in place the $250,000/$500,000 exclusion of gain from the sale of a principal residence. Also, the taxation of unrealized gains at death won’t affect assets held in IRAs, 401(k)s and other qualified pension plans, or 529 accounts. And it’s only a tax on gains—not on basis. The upshot is that most individuals (couples) will be able to pass substantially more than $1.25 million ($2.5 million) to beneficiaries at death without having to worry about federal income tax.

Biden’s stepped-up basis reform is sometimes described as “repeal” of stepped-up basis, but that’s not quite right. Assets transferred at death still will have a basis going forward equal to fair market value at the time of death. What will change (if Biden’s proposal passes) is that the decedent’s estate (or a nongrantor trust) will owe tax on the unrealized gains. In this respect, Biden’s plan differs meaningfully from previous attempts at a carryover-basis-at-death regime.